Table Of Content

An important part of the home buying process for buyers is knowing how much house they can afford. Generally, you’re better off using a mortgage calculator to calculate your mortgage payment because it’s difficult to input the formula properly in a regular calculator. Using the above calculator can help you put together all of these complex variables to get a clear picture of your monthly mortgage payment so you know exactly how much to expect. There are several factors that determine your interest rate, including your loan type, loan amount, down payment amount and credit history. Mortgage refinance is the process of replacing your current mortgage with a new loan.

What documents should I keep after paying off my mortgage?

Rent vs Buy Calculator: Should I Rent or Buy? - NerdWallet

Rent vs Buy Calculator: Should I Rent or Buy?.

Posted: Thu, 30 Nov 2017 02:18:43 GMT [source]

The length of your mortgage terms dictates (in part) how much you’ll pay each month—the longer your term, the lower your monthly payment. Along with calculating how much you expect to pay in maintenance and other house-related expenses each month, you should also consider your other financial goals. For example, if you’re planning to retire early, determine how much money you need to save or invest each month and then calculate how much you’ll have leftover to dedicate to a mortgage payment. Using a mortgage calculator takes the guesswork out of the formula and can help you calculate your mortgage payments much faster. There are several types of mortgage calculators, so it’s important to understand the purpose of each one so that you can be sure you’re using the right one for your needs.

Next steps: Start the home loan process

Reducing the amount you need to borrow, even by a little bit, will lower the amount you pay in interest over time, and it can lower your monthly payments as well. Ideally buyers would be able to put down at least 20% of the home price to avoid paying private mortgage insurance, but it’s not a requirement. With the median home price in 2023 at over $425,000, the average homebuyer would need $85,000 just for the down payment. Credit card issuers aren't required to give advanced notice of an interest rate increase for credit cards with variable interest rates.

Property Taxes

Pokemon cards have seen a "massive surge", Tracy says, with people paying "thousands and thousands of pounds" for good unopened sets. The information herein is general and educational in nature and should not be considered legal or tax advice. Tax laws and regulations are complex and subject to change, which can materially impact investment results.

Free home loan calculator: Estimate the monthly payment breakdown for your mortgage loan, taxes and insurance

If you can comfortably pay this, you might be able to afford a $300,000 mortgage. As you play around with the calculator, you can see how different down payment amounts will ultimately impact your monthly payment. The less money you borrow, the less you'll need to pay each month. To determine how your second monthly payment breaks down, simply subtract the $271 from your principal and run the calculation again with the new loan amount.

What is the average down payment for a house?

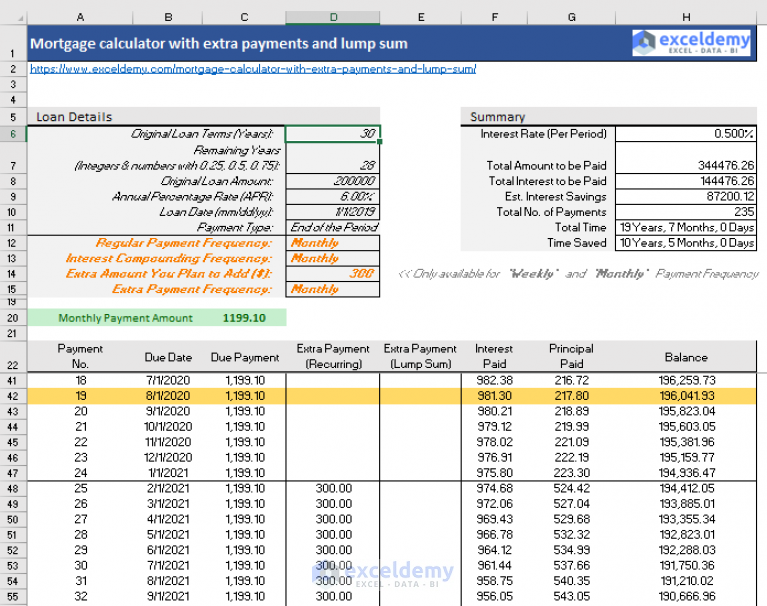

Another strategy for paying off the mortgage earlier involves biweekly payments. This entails paying half of the regular mortgage payment every two weeks. With 52 weeks in a year, this approach results in 26 half payments. Thus, borrowers make the equivalent of 13 full monthly payments at year's end, or one extra month of payments every year. The biweekly payments option is suitable for those that receive a paycheck every two weeks. In such cases, borrowers can allocate a certain amount from each paycheck for the mortgage repayment.

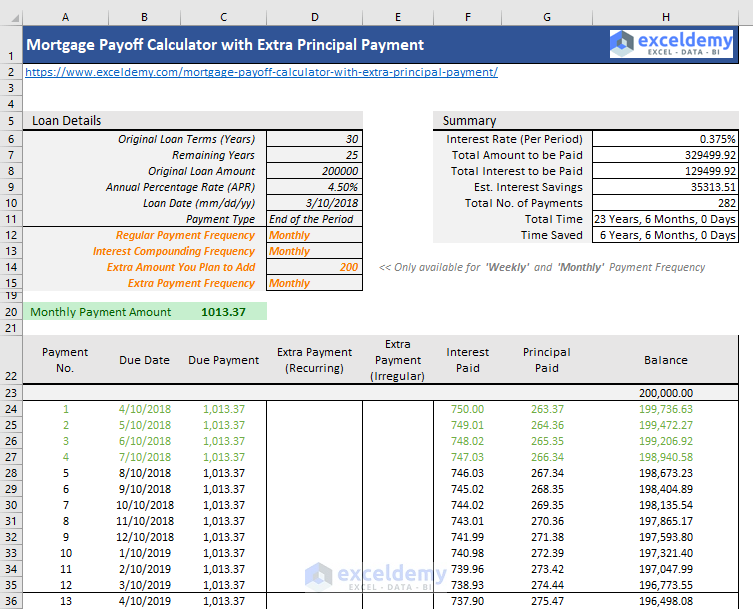

Mortgage Payoff Calculator

Broadly speaking, variable rates are more favorable to the borrower when indexed interest rates are trending downward. Another option involves refinancing, or taking out a new mortgage to pay off an old loan. For example, a borrower holds a mortgage at a 5% interest rate with $200,000 and 20 years remaining. If this borrower can refinance to a new 20-year loan with the same principal at a 4% interest rate, the monthly payment will drop $107.95 from $1,319.91 to $1,211.96 per month. The total savings in interest will come out to $25,908.20 over the lifetime of the loan.

The answer depends on several factors including your interest rate, your down payment amount and how much of your income you’re comfortable putting toward your housing costs each month. Assuming an interest rate of 6.9% and a down payment under 20%, you’d need to earn a minimum of $150,000 a year to qualify for a $400,000 mortgage. That’s because most lenders’ minimum mortgage requirements don’t usually allow you to take on a mortgage payment that would amount to more than 28% of your monthly income. The calculator also allows you to get a more detailed cost estimate by adding any homeowners insurance, mortgage insurance or homeowners association (HOA) fees you might pay for the house.

It includes advanced features like amortization tables and the ability to calculate a loan including property taxes, homeowners insurance & property mortgage insurance. The mortgage payment estimate you’ll get from this calculator includes principal and interest. If you choose, we’ll also show you estimated property taxes and homeowners insurance costs as part of your monthly payment. Because your lender benefits when you pay your property taxes and homeowners insurance, it typically will include these costs in your monthly mortgage payment. If inflation continues, mortgage rates could go up - increasing the monthly cost of the average American home. Moreover, with some buyers waiting for lower mortgage rates before they enter the market, you may have less competition to contend with, which could mean you'll save money on the price of your home.

Non-conforming loans are not limited to the size limit of conforming loans, like a jumbo loan, or the guidelines like government-backed loans, although lenders will have their own criteria. You don't need to borrow the full amount a lender is willing to lend to you. For example, if your lender offers you a loan for $300,000 but you only borrow $270,000, you could potentially save around $200 per month. Rates vary among mortgage lenders, so be sure to get approved with three or four different lenders to be sure you're getting the lowest rate possible. Lenders have a responsibility to make sure they aren't lending more than what their borrowers can afford to pay back.

NerdWallet’s mortgage payment calculator makes it easy to compare common loan types to see how each type of loan affects your monthly payment. We source the latest weekly national average interest rate from Zillow, so you can accurately estimate and compare your monthly payment for a 30-year fixed, 15-year fixed, and 5/1 ARM. Conventional loans are backed by private lenders, like a bank, rather than the federal government and often have strict requirements around credit score and debt-to-income ratios.

You can also see what the effect of a one-time, monthly or yearly additional payment would be on your number of monthly payments or interest. It’s factored into your monthly payment and paid off throughout the life of your loan. A down payment of 20% or more will get you the best interest rates and the most loan options. There are a variety of low-down-payment options available for home buyers. You may be able to buy a home with as little as 3% down, although there are some loan programs (such as VA loans and USDA loans) that require no money down.

An amortization schedule shows you how much of your payment goes toward paying off principal and how much goes toward interest for any given payment you make. At the beginning of a loan, more of your payment goes toward paying interest than paying down your principal. Getting the best interest rate that you can will significantly decrease the amount you pay each month, as well as the total amount of interest you pay over the life of the loan.

These down payment assistance programs may offer help in the form of forgivable grants and low-cost loans. The programs are designed to encourage homeownership and are generally restricted to first-time homebuyers. In general, you may qualify for a better interest rate with a higher down payment, which reduces the overall cost of your mortgage over time. Even a .25% reduction in your interest rate could save you thousands of dollars over the life of your loan. The down payment is the portion of the home’s purchase price that you pay upfront and is not financed through a mortgage. The down payment directly reduces the amount of money you need to borrow for the home purchase.

What if you’re not looking to move to a new place, but instead looking to refinance your current home? The first question a refinance calculator will ask you is what your goal is with a refinance. For example, you might wish to lower your existing loan payment, pay off your mortgage faster or take cash out. As mentioned above, the easiest way to come to your mortgage payment is to use a mortgage calculator. However, having a basic understanding of the formula can give you an idea of how changing variables impacts the other parts of the equation. For your convenience current mortgage rates are published underneath the calculator to help you make accurate calculations reflecting current market conditions.